In recent weeks, we have seen a lot of reportings in the local dailies on cotton sourcing and the difficulties that our textile industry's stakeholders are facing. Almost all of them reported subjectively and some made overly simplified statements that do not necessarily describe the realities, causing significant anxieties and frustrations among the stakeholders. It is important to realise that the textile industry is the core element of our economy. This is the industry, which earns 76 per cent of our foreign export income and hence is vital for our economy and national security. Stakeholders must have access to objective reports and analyses that would help them understand the actual situation in cotton and textile market and make appropriate decisions for their companies in a timely manner. This current report attempts to address this issue.

The cotton season for countries in northern hemisphere starts in October and countries in the southern hemisphere starts in April. More than 90 per cent of cotton produced in the world are in the countries of northern hemisphere, including China, India, the USA, Pakistan, Africa, Uzbekistan and other Central Asian countries. Therefore, October is significant for cotton production and use. Last month, we witnessed a record rise in cotton price in the history of cotton industry. On October 11th, the Cotlook A-Index (the price of five cheapest varieties of cotton and is daily published by Cotton Outlook, a Liverpool based marketing research group, broke its previous record of 119.4 US cents per pound, which was established on April 27, 1995. And the New York Futures also sets a record at 110.50 cents per pound.

As we write this report on November 5, 2010, the A-Index hits 160 and the ICE Index rose to 142.3 cents per pound, which are new records for both indices. The International Cotton Advisory Committee (ICAC) reported that the Cotlook A Index averaged 127 cents per pound in October, 21 per cent more than in the previous month and 89 per cent higher than in October 2009.

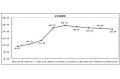

INSERT A: New York ICE index for 2007-08, 2008-09 and 2009-10 cotton- season. The 2007-08 and 2009-10 seasons show two different market responses.

The end of 2009-10 cotton season endured a few dramatic events that had tremendous impacts on the market. The Indian ban on cotton was imposed in April 2010, which did not immediately affect the New York ICE market except for slight volatilities later. However, the Pakistan flood report, along with the Chinese bad crop report, moved the market to an upward trend with more volatility. Then in October, the news from India revealed a limit in export volume of 930,000 tonnes. The International Cotton Advisory Committee reported an export volume of about 1.03 million tonnes from India. Therefore, the Indian government export limit falls 100,000 tonnes short of the ICAC estimated export volume. The ICAC estimated that the Indian crop size would reach to a record 5.72 million tonnes in 2010-11 season and the mill use would reach to a record 4.56 million tonnes, resulting a surplus of 1.16 million tonnes and an end of the year stock change by 230,000 MT.

INSERT B: Global Cotton Consumption and Use, 2006-07 through 2011-12 (Projected). Nearly 3.0 trillion tonnes of cotton fell short in 2009-10.

and

INSERT C: Global Ending Stocks, 2006-07 through 2011-12 (Projected). The Chinese and USA stocks dropped to a record low in 2009-10.

Low global cotton stock and continued demand by spinning mills caused a steep rise of cotton prices. The cotton world has been comfortable with an ending stock of about 12 million tonnes. In 2009-10, the global cotton stock fell by 25 per cent or 8.9 million tonnes, the smallest in seven years. The Chinese and USA stock also dropped to a record low with a little sign of recovery for the next few years. On the other hand, according to the International Cotton Advisory Committee, the cotton demand increased by 5.0 per cent to 24.6 million tonnes.

If we compare the 2009-10 cotton market with 2007-08, both seasons reveal completely different scenarios. Right after the commodity market collapse in March 2008, the market took a downward roller coaster ride with greater uncertainty for the rest of the season.

That was the same period when the cotton world watched the three giant cotton companies collapsed. A number of small to medium size cotton companies went out of business around the world. Those companies who managed to survive were bruised badly and are still recovering the big losses incurred. It did not fare well for Bangladesh because the Bangladesh textile industry heavily dependent on those companies for their cotton. These companies traditionally have been playing an important role in the supply chain of textile mills.

It is therefore the interest of both textile mill owners and international merchants to develop a better understanding and working relationship. Never in history, the Bangladesh textile industries took the opportunity to develop closer working relationship among the mill owners and merchants.

In that respect, the 2009-10 season did not harm our industry much except for the price hike. However, it gave us enough indications that the market would climb up for a considerable amount of time. Smart mill owners took their position well ahead of time, but those who were wondering around had a difficult time securing their cotton. It was the first time in our textile industry's history we realized that the source of cotton, not its price, was the main problem.

Sourcing Cotton

With all these difficulties, Bangladesh seemed to manage sourcing its cotton fairly well. In 2010, from January through September, Bangladesh imported 37 per cent of its cotton from Uzbekistan, 29 per cent from India, 12 per cent from Africa, 8 per cent from USA, 5 per cent from Turkmenistan and 9 per cent from other countries. Four years ago, however, the dynamics were different. Uzbekistan had a large presence in Bangladesh market with an impressive 65 per cent market share. Unfortunately, it lost its market share to India, which shows a strong growth in market share from 10 to 29 per cent in four years.

INSERT D: With all these difficulties Bangladesh Seemed to manage sourcing its cotton from different countries. Jan - Sep, 2010

and INSERT E: Four years ago the dynamics of market share in Bangladesh was quite different. Uzbekistan had mighty presence in Bangladesh market with an impressive 65 per cent market share in 2006

Uzbekistan, a high quality producer of cotton, and India, a next-door neighbour, have been playing an important role as cotton sourcing countries for Bangladesh. The increase in Indian market share in Bangladesh in last four years, however, demonstrated a natural strategic alliance between the cotton industries of both the countries. It is important that our industry leaders understand the Uzbekistan and Indian cotton markets with greater details.

INSERT F: Dynamics of Cotton Imports from Uzbekistan and India, 2008-2010.

The numbers of Uzbekistan and India's exports to Bangladesh show an interesting pattern. It seems obvious that India has been very competitive throughout the year. However, their market share usually declines between March and August, when quality of Indian cotton declines significantly. During the rest of the season, the Indian market share increases only when the quality is fairly good and comparable to Uzbekistan cotton. It is true enough to say that Uzbekistan and Indian market shares are highly inversely correlated.

When Indian cotton market share ascends, the Uzbekistan market share falls. However, the 2010 dynamics are quite different. We do not see the seasonality in the dynamics of imports from Uzbekistan and India.

Early this year, the Uzbekistan supply was tight; hence, the Indian supply rose significantly. It reached to a high level of over 50,000 tonnes per month right before the Indian ban on cotton export. Since then, the Indian market share declined, and Uzbekistan did not recover the market because of its tight supply.

INSERT G: Indian Exports and Surplus between 2006-07 and 2011-12 (Projected).

In 2007-08, India exported more cotton in the global market than its surplus (production minus domestic use). In 2008-09, however, they stepped back and exported at least 0.5 million tonnes less than their surplus level. The Indian export went up to 1.4 million tonnes in 2009-10 cotton season, exceeding their surplus level of 0.8 million tonnes. With a surge in export and under pressure from the Indian mills association, Indian Government placed a ban on export in April 2010. In the current season of 2010-11, the Indians put a limit on their export to about 930,000 tonnes, which is short of their export potentials of 1.16 million tonnes.

So, where should we look for cotton? We should pay attention on primarily three different growths, Uzbekistan, India and Africa. These growths are better quality, cheaper and more cost effective. Uzbekistan grows a few of the best varieties of cotton in the world, and their cotton offers better spinability. Unfortunately, in recent years, the supply from Uzbekistan has been getting tighter because their domestic use is increasing and Chinese companies are buying cotton from Uzbekistan in a bigger way. Bangladesh currently faces intense competition in Uzbekistan.

India provides an excellent alternative to Uzbekistan growth because of better and consistent quality every year and competitive prices. India has the potential to be a strategic source for Bangladesh for several reasons. India is our next-door neighbour, is the second largest producer of cotton in the world, and can grow more cotton in plenty of farmlands. They have modernised their cotton farming and ginning industry and improved their quality significantly in last few years. The major problem with Indian growth is the political interference, which has occurred in recent months and undermines our dependability on a single source.

African countries (both West Africa and East Africa) also provide an excellent potential for becoming a strategic source for Bangladesh. Unfortunately, the total volume of production from Africa is very limited. Unlike India, this source does not pose any political threats on export. Logistics and transportation have always been a challenge for cotton exporters from Africa.

Other countries, like the USA, Brazil and Australia, also have been consistent source for Bangladesh, which should continue to source cotton from these countries. Although these growths provide contamination-free and excellent quality varieties, they are very expensive and take a longer time to ship to Bangladesh. In addition, Bangladesh faces intense competition for these growths with Far East countries, including Korea, Indonesia, Taiwan, and China.

A wakeup call

The 2009-10 cotton season gave us a wakeup call to prepare ourselves for the future. It gave us a realisation that Finding Cotton is an issue but not the Price. It reminded us that our Textile Industry is vulnerable to foreign sources, whereas the 2007-08 cotton season did more harm to our industry than 2009-10 season.

This is the season when some of the largest cotton companies in the world went out of business. Also, a few small to medium size companies declared bankruptcy, and the textile industry lost support from these merchants who have been playing important role in supplying cotton. Bangladesh textile industry is vulnerable because Bangladesh does not produce cotton and depend on 76 per cent of our earning on textile industry. This is more of an issue of national security than a cotton security.

There are two major challenges Bangladesh textile industry is facing: external and internal. The external problems are the geopolitical and logistical, and the internal challenges are institutional. Any disruption in supply and demand chain in textile industry are intrinsically linked to economic and national security of Bangladesh.

Events, even as small as port congestions or as major as disruptions in the sourcing countries including geopolitics, weather, or any political decisions, may have adverse effects on the export and import trades of textiles in Bangladesh. Bangladesh must develop an institution that can look at the geopolitical risks in sourcing raw cotton, a key raw material that feeds the backbone of our economy.

This institution would also evaluate possible interruptions in supply chain of raw cotton, which are serious national security issues. An alternative plan based on various scenarios should be in place that would ensure an uninterrupted supply of raw materials to the textile industry.

We propose that a strategic reserve of two to three month supply of raw cotton can provide a first line of defence against an unexpected interruption in supply chain.

We would not suggest that the government should step in and make this reserve because this challenge should be left for the industry. We are confident our industry alone, with a little political, diplomatic, banking and institutional help from the government, can handle this obstacle.

This is a perfect time for Bangladesh to encourage its companies to merchandise raw materials including cotton, invest in foreign cotton producing countries including the set up of ginning factories, and trade cotton directly from foreign farmers or government agencies. Companies should be able to trade cotton all over the world. If the Bangladesh companies can secure cotton from international producers, Bangladesh mills would be better secured.

The major internal threat is the absence of institution that can train and employ cotton experts, economists and statisticians. A well-established institution is necessary where economists and scientists can study cotton market and give direction to our industry leaders and policy makers, who are facing unprecedented challenges. Therefore, we strongly suggest that a National Textile Council (NTC) be formed through a public and private partnership effort. The council should comprise of five major industry associations: Bangladesh Textiles Mills Association (BTMA), Bangladesh Cotton Association (BCA), Bangladesh Garments Manufacturer and Exporters Association (BGMEA), Federation of Bangladesh Chamber of Commerce and Industries (FBCCI) and the Government. The NTC, as a think tank, can perform research on cotton markets, cotton sourcing, and textile markets. The NTC would also employ world-class economists, statisticians and scientists. Members would regularly participate in international forums, gain experience, develop professional connections with world industry leaders, study and develop new markets. They would also examine and understand the strength and weakness of our industries as well as our competitors and develop programs to create more experts and leaders who will provide leadership and technical direction to policy makers and industry leaders.

While Bangladesh textile industry needs to be active in a number of international and national issues, participation in the international forums would provide a strong voice to our industry and would raise concerns and resolve issues with our strategic partners. We would like to see a collaborated effort by all the major cotton and textile associations of the Bangladesh, who would organise conferences and seminars. They should also seek membership with the International Cotton Advisory Committee (ICAC), International Cotton Association (ICA), Indian Cotton Association, and other important international forums. This kind of participation will allow us to brainstorm ideas for all the parties who have stakes in the development of our textile industry. It will also allow us to interact with international experts, who have foremost knowledge of international issues. Their information may directly or indirectly affect on how we compete in the world market.

Diplomacy

The Hasina administration demonstrated a strong leadership to ensure an uninterrupted supply of raw materials for our textile industry. A recent visit of Mr. Faruk Khan, Minister of Commerce, to India reflects the administration's commitment to ensure a secured supply of raw cotton. We now know that the Indian government is committed to provide us additional 180,000 tonnes (1.1 million bales) of cotton this season, leaving a positive impact on our industry. We hope that the scheduled visit of Minister Faruk Khan to Uzbekistan will also bring some encouraging news for textile industry. We sincerely hope that the Administration will continue to seek diplomacy to resolve the challenges we are facing in sourcing our raw cotton.

Dr. Quamrul Ahsan is the Editor-in-Chief of Cotton Bangladesh, an international cotton magazine published from Bangladesh. Mr. Saquib Ahsan is a business graduate from Cornell University, New York and works for Cotech, Inc. a New York-based company stationed in Dhaka.