Export heads toward growth

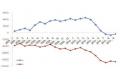

In the Jan.-Apr. 2010 period, China's textile and garment total exports amounted to $55.3 billion, up 15.76 percent y/y, slightly increasing by 25.92 percentage points from the growth rate of the Jan.-Apr. 2009 period. Of which, textile exports jump 25.90 percent to $23.108 billion; Garment exports jump 9.44 percent to $32.192 billion.

Looking further into the destination, textile and garment exports to the U.S. increased by 20.61% y/y in the Jan.-Apr. 2010 period, up 21.81% from the growth rate of the Jan.-Apr. 2009 period; Exports to Japan decreased by 3.67% y/y in the Jan.-Apr. 2010 period, down 8.08% from the growth rate of the Jan.-Apr. 2009 period; Exports to ASEAN increased by 37.23% y/y in the Jan.-Apr. 2010 period, up 45.84% from the growth rate of the Jan.-Apr. 2009 period.

Table. Growth rate of China textile and apparel exports by destination

|

Period |

Total |

To the U.S. |

To EU |

To Japan |

To AESAN |

To Africa |

To Oceania |

|

Jan.- Apr. 2008 |

17.04% |

1.82% |

40.40% |

7.39% |

39.28% |

20.87% |

25.55% |

|

Jan.-Apr. 2009 |

-10.16% |

-1.20% |

-11.28% |

4.41% |

-8.61% |

-7.96% |

-9.70% |

|

Jan.-Apr. 2010 |

15.76% |

20.61% |

16.34% |

-3.67% |

37.23% |

22.18% |

15.32% |

Source: China Customs

Europe's fragile and slow recovery

In early 2010 fears of a sovereign debt crisis or the 2010 Euro Crisis developed concerning some countries in Europe including: Greece, Ireland, Spain and Portugal. This led to a crisis of confidence as well as the widening of bond yield spreads and risk insurance on credit default swaps between these countries and other EU members, most importantly Germany.

Concern about rising government deficits and debt levels across the globe together with a wave of downgrading of European Government debt has created alarm in financial markets. The debt crisis has been mostly centered on recent events in Greece, where there is concern about the rising cost of financing government debt.

European debt crisis and the consequent sovereign credit risk of developed economies and a new round of global financial market turmoil have limited direct impact on China, but indirect effects can not be ignored. Affected by the debt crisis, the euro fell against the dollar to 14-month low. The recent sharp rise in the renminbi exchange rate against the euro makes the situation of China's exports to Europe more and more severe.

World economy is recovering

The world economy is recovering steadily but the pace of recovery is very slow. There are many uncertain factors. The industry needs to prepare for future difficulty. The debt crisis in some European countries may impede Europe's economic recovery and bring change to European markets.

Global manufacturing expands at fastest pace since 2004. The JP Morgan PMI rose to 57.8 in April. Output and new orders surged to multi year highs.

USeconomy continues to improve. The surprise surge in US factory orders confirmed the manufacturing sector continues to lead the recovery. Details were strong. Excluding transportation orders, factory orders surged 3.1 percent, the biggest gain in five years, whereas non-defence capital goods (ex-aircraft) jumped by 4.

5 percent. While the climb in pending US home sales to a five month high is largely due to homebuyer tax credits, analysts believe it bodes well for the coming months. Analysts expect April US non-farm payrolls to increase by 200k, but an upward surprise is definitely possible. However, according to Former FOMC Chairman Paul Volcker, it could be a "long slog" as the economy struggles to reduce the jobless rate (currently 9.

7 percent).

Eurozone's Apr manufacturing PMI comes in slightly above the flash 57.5 reading, at 57.6, signalling a pick up in sector activity rates in the initial stages of the second quarter (Mar: 56.6, 4cast & Mkt: 57.5). The result follows similarly positive readings from both Germany (61.5 vs. flash 61.3, Mar 60.

2) and France (56.6 vs. flash 56.7, Mar: 56.5) although there are signs that momentum is starting to ease off after the initial impulse higher. It's not just the German-Franco engine that is driving the revival, indeed preceding PMI surveys within the bloc suggest that even the 'structurally-laden' member states are starting to gain gusto with Spain's PMI index hitting the highest since June '07 (export orders at a decade high) with Italy PMI also up; 54.

3 vs. 53.7. The question over sustainability has plagued recovery views, but for the first time there are signs that sector activity is starting to form a sustainable base. The rise in input costs (54.4 vs. Mar's 49.9) may weigh on firms ability to remain cost-price competitive but experts believe this has been enhanced by the weakness of the Euro rate especially within the commodity sphere.

Asiaeconomy continues to improve. Singapore's economy grew 15.5 percent in the first quarter from a year earlier, up from its initial estimate of 13.1 percent, led by the manufacturing sector; The Thai economy grew by 12 per cent year-on-year in the first quarter, the highest growth rate in the past fifteen years for Thailand; China's economy expanded 11.9 percent year on year in the first quarter, indicating a solid recovery of the world's third largest economy, but also fanning concerns of asset bubbles.

Keeping a watchful eye on debt crisis

Some analysts have pointed out that the European economic outlook is not promising, a large number of hot money may turn to flow into emerging markets like China, and this will aggravate the pressure of RMB appreciation and the risk of economic overheating in China.

The effects of Europe's debt crisis are starting to filter down to Chinese textile exporters. Some are already noticing a decline in orders from Europe. Now experts are warning companies to brace for a longer term impact. Compared to large export firms, small and medium companies face more pressure. The changing currency exchange rate can dramatically cut their profits. Companies should prepare for further exchange rate risks.

Related News

Photos

More>>

trade

- Analysis of economic performance of China's cotton spinning industry in Q1-Q3

- Intertextile - successful event; launch of new show next year

- Dow Corning to exhibit textile innovations at Intertextile

- Cinte Techtextil opens next week with 310 exhibitors

- AMANN to show techX Performance Threads at Intertextile

market

finance

- FDF: Resolve legal limbo on 'no added salt' claims

- Change4Life didn't change anything, claims academic

- Vice Minister Zhang Taolin Focuses on Innovation of Management Mechanism and

- Minister Han Changfu Meets with Italian Minister of Agriculture, Food and

- Vice Minister Zhang Taolin: Promote the Development of Seed Industry