Light vehicle sales grew a mere 5 percent last month over July 2010 and fell 10 percent from the previous month June.

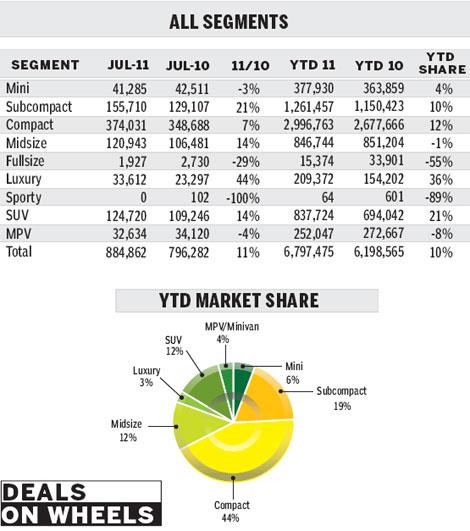

Though passenger vehicle sales increased 12 percent year on year to 953,000 units, light commercial vehicle sales fell 12 percent in the period to 305,000 units.

Due to a convergence of factors, the passenger vehicle market was stronger than normal for July, traditionally a weak month because hot days reduce overall activity and showroom traffic.

Most carmakers, including Shanghai VW and Chang'an Ford Mazda, build up inventories in June, which allows them to cut shifts in July and give "high temperature leave" to workers.

But there were exceptions this year.

After losing market share in the second quarter, Japanese carmakers didn't waste the opportunity to make up for lost volume, so they ran at full capacity to complete the backlog and fill inventory at dealers.

Toyota hit historically high volumes, while Honda's production returned to normal.

Price war

A price war initiated by Japanese brands also greatly stimulated retail sales.

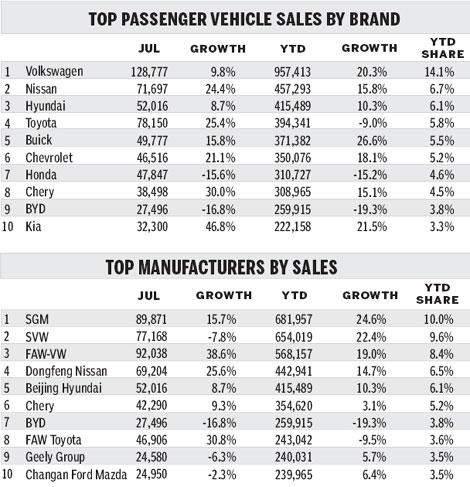

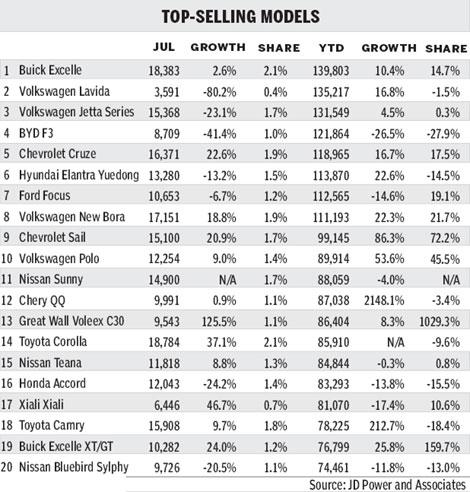

The strong performance by mid-sized cars, which grew 14 percent year on year, was the result of large incentives offered on the Accord, Camry, Teana and Reiz.

Reluctant as other carmakers might be - especially Korean brands whose new Sonata and K5 just arrived on the market a few months ago - they had to answer with discounts despite the fact it could hurt their brand image.

The discount war also hit other segments with the average transaction price in all segments except SUVs and sub-compact cars falling July.

As a result, local brands such as BYD, FAW and SAIC all recorded double-digit declines. Geely saw its lowest sale volume in 24 months.

Total sales by Chinese brands only rose 5 percent year on year, compared with global brands that achieved 15 percent growth.

In the first seven months, Chinese brand share of the passenger vehicle market declined 1.6 percent to 30.5 percent.

Declining sales, increasing incentives and rising material and labor costs are making low-cost carmakers such as Chery and BYD struggle for profits.

Fortunately, soaring export demand, which accounted for nearly 10 percent of the total wholesale volumes of the Chinese brands, somewhat offset their sluggish domestic demand.

With an increasing numbers of models and improving quality, made-in-China cars are becoming more and more popular in overseas markets.

Sales have also been slow due to the end of the major tax incentives of last year and purchase restrictions to curb traffic congestion.

The government's monetary tightening and high inflation may be also dampening consumer willingness to buy new vehicles. Recent downgrades in the US and European economic outlook also presents a major risk to China's economy and its export growth prospects.

As a result of the various economic factors, we have downgraded our forecast for light vehicle sales for the year to 17.7 million units from the previous projection of 18.1 million units.

Passenger vehicle sales are forecast to grow 8 percent to 12.9 million units, while light commercial vehicle sales are projected to decline 9 percent year on year to 4.8 million units.