Hindsight is always a great thing. It explains, in a lot of situations, what foresight could have prevented.

How often do we hear people saying, "Oh, if only I had bought a home before prices surged!" or "Why didn't I sell those shares at their highs?"

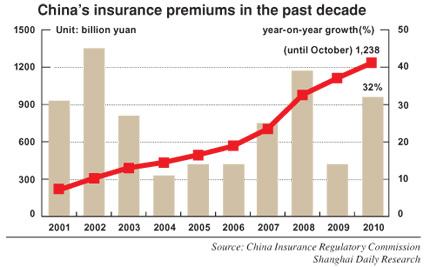

Oddly this retrospective insight into our human frailties doesn't seem to help much where the insurance industry is concerned.

The apartment complex blaze that killed at least 58 people in Shanghai on November 15 is a case in point. It turns out only a handful of residents had insurance policies covering their homes and contents. Insurance compensation can't bring back the life of a loved one, but it can go a long way in staunching the kind of material losses almost all of the families now face.

The combined property losses of the reported 156 families living in the building have been estimated at 500 million yuan (US$75.2 million), based on the average market price of 30,000 yuan per square meter for residential space in the area, said earlier media reports. By November 23, insurers in Shanghai paid more than 8.3 million yuan in claims related to the fire, according to the Shanghai Bureau of the China Insurance Regulatory Commission, the nation's top industry regulator.

Of the 8.3 million yuan, 5 million yuan came from a publicly financed community insurance fund, indicating the low penetration of the private insurance sector.

Life, property and casualty insurance is still a relatively new concept in China. I still remember the sneer from one of our business reporters, a frequent flier, who was asked if he bought flight insurance. "What's the use of money if one is dead?" the reporter replied.

That misses the point. Insurance aims to provide relief for survivors in case of death.

I did a quick, informal survey among 12 colleagues on the subject of buying insurance. Only one said he has insurance to protect his family from "the uncertainties of the future."

"I bought insurance to cover illness, pension and accidents," said the 30-year-old married guy, whose monthly salary is around 7,000 yuan. "I don't want my family to suffer a deteriorating quality of life if anything happens to me."

The other 11 all said they had no insurance at all, including a reporter covering the insurance industry.

"My own experiences showed me that insurance agents are always quick to boast about all the things they can offer when they are selling policies, but when it's time to file a claim, it's a tedious and complex process to try to collect on any of those promises," said the mother of a three-year-old boy, recalling her unhappy experiences when she claimed reimbursement under the employer's group medical policy.

Difficulty in claiming compensation, the lack of third-party agencies to provide an impartial guide to insurance products and lack of trust in insurance professionals have topped the list of why my colleagues aren't rushing out to buy insurance.

Hu Shi, the esteemed Chinese philosopher and essayist who died in 1962, once said that insurance is to prepare for tomorrow today, prepare for death while one is still alive, and prepare for children when you're parents.

His wisdom seems to be particularly well received by the well-off.

It appears the more money you have in China, the more you are aware of insurance protection. Buying protection to cope with major diseases, protect pension funds and savings, and guarantee enough money for children's education top the list of needs when the wealthy consider their risks, according to a survey conducted by HSBC Life Insurance Co.

The survey centered on people in Shanghai, Guangzhou and Beijing who had financial assets of 500,000 yuan or more.